Ever wondered why your friend got a home loan approved in two days while yours is still stuck? Or why your neighbour got a lower EMI and interest rate compared to you ? Or why some people get those “Pre-approved” credit cards with zero effort?

The secret is in that 3-digit number: Your Credit Score.

In India, we often call it our “CIBIL Score,” but whether it’s from CIBIL, Experian, or Equifax, it’s basically your financial report card. It tells banks if you’re a “Total Rockstar” (900 points!) or if your credit profile is weak and risky (closer to 300).

Credit scores can feel confusing, but you don’t have to navigate it alone. FreeCreditReport.in is your ‘Financial Dost’—giving you clear answers, help you gain free access to your reports, and the exact steps to turn your score around.

-

We explain what the credit score is and what it actually says about your financial health. From “High Risk” to “Credit King,” we translate the jargon into a plan you can use.

-

The Right to Free Access: Every Indian is entitled to one Free Full Credit Report per year from each of the four major bureaus (CIBIL, Experian, Equifax, and CRIF). We show you exactly how to claim yours directly from the official sources without the “hidden charges” or “convenience fees” others might slip in.

-

We’ll show you why your CIBIL score might differ from your Experian report so you’re never in the dark when a lender checks your profile.

-

If your score is low, don’t sweat it. With 2026’s new weekly reporting rules, your good habits show up faster than ever. We’ve got the exact steps to help you pull it up and get that loan approved.

Think of us as your personal guide to making smarter money moves.

Why Your Credit Score is the Secret to Saving Lakhs

We’ve all heard the term “CIBIL Score” thrown around by bank agents and SMS alerts. But is it just a random number, or does it actually impact your wallet?

In 2026, the answer is more critical than ever. Your credit score is no longer just a “pass or fail” mark for a loan; it is the ultimate bargaining chip that determines how much interest you pay. Think of it as a “Reputation Discount”—the better your track record, the less the bank charges you.

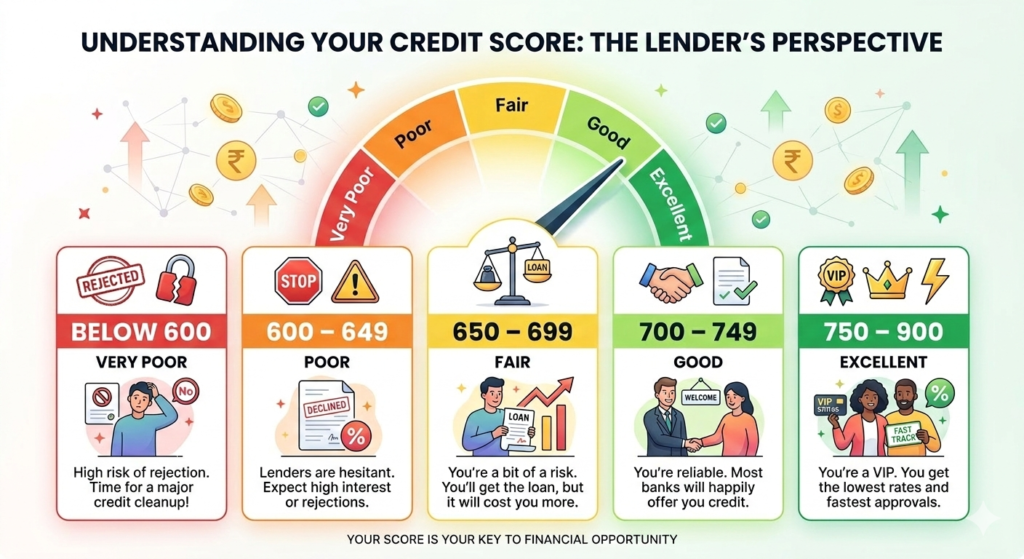

The Scorecard: Where Do You Stand?

In India, credit scores range from 300 to 900. This three-digit number tells a lender how likely you are to repay your debt on time.

Pro Tip: Aiming for a score of 750+ is the “sweet spot” to unlock the best financial products in India.

How Your Score Directly Changes Your Interest Rate

Major Indian banks like SBI, HDFC, and ICICI use Risk-Based Pricing. They don’t have one single interest rate for everyone. Instead, they “tax” you for a lower score.

-

The “Prime” Treatment (Score 750+): You get the bank’s lowest advertised rate.

-

The “Risk Premium” (Score 650–749): Banks may add a 0.5% to 1.5% surcharge to your interest rate because they view you as a moderate risk.

-

The “Subprime” Penalty (Below 650): If you aren’t rejected outright, you could face rates 2% to 5% higher than a Prime customer. On credit cards or personal loans, this gap can be even wider!

The Real-Life EMI Impact: A ₹7.7 Lakh Mistake?

Let’s look at a 20-year Home Loan of ₹50 Lakh. A small difference in your score can lead to a massive difference in your bank balance:

-

With an 800+ Score (8.50% Rate): Your EMI is ₹43,391.

-

With a 650 Score (9.50% Rate): Your EMI jumps to ₹46,607.

The Result: You pay an extra ₹3,216 every single month. Over the life of the loan, you lose nearly ₹7.7 Lakhs simply because your credit score was lower. That’s money that could have gone toward your retirement or your child’s education!

The 2026 Game Changer: Weekly Reporting

The rules changed in April 2026. Per the latest RBI mandate, banks now report your data to credit bureaus every week instead of once a month.

-

The Good News: If you pay off a big debt or fix an error, your score improves in just 7 days. You can negotiate a better “Balance Transfer” for your loan almost immediately.

-

The Warning: There is no “grace period” anymore. A single missed EMI will hit your report within a week, potentially hiking the rates on any new loan applications instantly.

Take Control Today

Your credit score is a living, breathing number. Whether you’re planning to buy your dream home or just want a premium credit card, keeping that score above 750 is the smartest financial move you can make.

Want to see where you stand? Check your latest report today and start your journey toward a “750+ life.”

What is a Credit Report and how can you get one ?

If the Credit Score is your “final grade,” the Credit Report is your “entire answer sheet.” It’s a comprehensive document that tracks every single loan, credit card, and EMI payment you’ve made over the last few years.

Here is a simple breakdown for your website on what’s in it and how Indians can grab theirs for free.

What exactly is a Credit Report?

Think of it as your financial identity. It’s a detailed record compiled by credit bureaus (like CIBIL) using data sent by your banks. It contains:

-

Personal Details: Your name, PAN, Aadhaar, and every address or phone number you’ve used with a bank.

-

Account History: Every loan (Home, Car, Personal) and credit card you own. It shows your “Current Balance” and “Credit Limit.”

-

The “DPD” (Days Past Due): This is the most important part. It shows if you were ever late on a payment by 30, 60, or 90+ days.

-

Enquiries: Every time you apply for a loan, it’s recorded here as a “Hard Enquiry.” Too many of these make you look “credit hungry.”

How to Get Your Credit Report in India

Under RBI rules, you are entitled to one full free credit report every year from each of the four major bureaus. Here are the three ways to get it:

1. The Official Bureau Websites (100% Free once a year)

Each of the four licensed bureaus in India must provide you with a free report. If you check one every quarter, you can monitor your credit for free all year round!

-

CIBIL: cibil.com

-

Experian: experian.in

-

Equifax: equifax.co.in

-

CRIF High Mark: crifhighmark.com

Read step-by-step instructions to access your free credit report from these bureaus.

2. Digital Apps & Fintechs (Free monthly updates)

Many Indian apps provide your credit score and a basic report for free every month because they want to offer you loans.

-

Popular Apps: CRED, OneScore, GPay, and Paytm.

-

Why use them? They are much faster and the interface is “human-friendly” compared to the technical bureau websites.

3. Financial Aggregators

Websites like Paisabazaar, BankBazaar, or Wishfin offer free reports from multiple bureaus simultaneously. They often give you a “Credit Health” summary which is easier to read than the raw data.

The 2026 Pro-Tip: The “Weekly Habit”

Since the RBI moved to weekly reporting in 2026, checking your report once a year isn’t enough anymore. Errors or missed payments show up in just 7 days.

Dost’s Advice: Use a free app to check your score at least once a month. It’s a “Soft Enquiry,” meaning it does not hurt your score, and it helps you catch errors before they cost you a loan approval!

CIBIL vs. The Others: Why Is My Score Different?

If you check your score on two different apps and see two different numbers, don’t panic! You aren’t being “downgraded.” In India, there are four RBI-licensed credit bureaus: TransUnion CIBIL, Experian, Equifax, and CRIF High Mark.

While they all receive the same data from your bank, your score varies because each bureau uses its own “secret recipe” (algorithm) to calculate your risk.

The Comparison: CIBIL vs. Experian vs. Equifax vs. CRIF

| Feature | TransUnion CIBIL | Experian / Equifax / CRIF |

| Market Role | The “Gold Standard” for traditional banks. | Preferred by Fintechs, NBFCs, and digital loan apps. |

| Score Range | 300 – 900 | 300 – 900 (Note: Experian sometimes uses 300-850) |

| “Excellent” Mark | 750+ | 800+ |

| Data Depth | Focuses heavily on bank loans and credit cards. | Often includes “Alternative Data” like utility bills or rent. |

| Update Speed | Historically slower, but moving to Weekly in 2026. | Known for faster API triggers and real-time updates. |

Why the Discrepancy Happens

-

Weightage of Factors: One bureau might penalize a “Hard Enquiry” by 10 points, while another only takes off 5. CIBIL often places a higher weight on repayment history, while Experian may look more closely at your credit mix.

-

Reporting Lag: Even with the 2026 Weekly Reporting mandate, Bank A might report to CIBIL on Monday and to Experian on Thursday. If you pay a big bill on Tuesday, your CIBIL score won’t show it for another week, but your Experian score might reflect it immediately.

-

The “New-to-Credit” Factor: If you are a first-time borrower, you might have a score on CRIF or Experian (due to a small “Buy Now Pay Later” loan) before CIBIL even recognizes you exist.

Which One Should You Trust?

There is no “most accurate” score—they are all valid. However:

-

If you are applying for a Home Loan or Car Loan from a major bank (SBI, HDFC, ICICI), focus on your CIBIL score.

-

If you are applying for an Instant Personal Loan or a Fintech Card (OneCard, Slice, Jupiter), your Experian or CRIF score is usually what they check first.

Why Your Credit Report Actually Matters (It’s Not Just About the Score!)

If your Credit Score is the headline, your Credit Report is the entire story. You might have a great score today, but without checking your report, you’re flying blind. Here’s why your report is the most important document in your financial kit:

1. It’s Your “Financial ID Card” for Banks

When you apply for a loan in India, the bank doesn’t just look at your 750+ score. They download your full report to see your repayment discipline. They check:

-

Have you been consistently late on EMIs?

-

Are you over-dependent on Credit Cards?

-

How many loans have you closed successfully? Your report proves you are a responsible borrower, not just a lucky one.

2. Catching “Ghost” Errors (The Silent Score Killers)

Indian credit bureaus handle data for over 400 million people. Mistakes happen! Sometimes:

-

A loan you closed 2 years ago still shows as “Active.”

-

A payment you made on time is marked as “Late.”

-

Your name or PAN is mixed up with someone else’s. If it’s on your report, it’s affecting your score. Regularly checking your report is the only way to spot these “ghosts” and get them fixed before you apply for a big home loan.

3. Protection Against Identity Theft & Fraud

With the rise of digital lending apps in India, “identity theft” is a real threat. Scammers might use your PAN card to take out a small “instant loan” that you know nothing about.

-

The Danger: You only find out when your score suddenly crashes.

-

The Solution: Your credit report lists every single enquiry and loan. If you see a bank name you don’t recognize, you can report it immediately.

4. The “Weekly Advantage” in 2026

Since the RBI’s 2026 Weekly Reporting rule, your report is now a “living document.” In the old days, you could fix a mistake and wait a month for it to clear. Now, you can see changes in just 7 days. Monitoring your report weekly allows you to move fast—whether it’s fixing an error or showing a bank that you’ve just paid off a credit card to get a better interest rate.

Dost’s Summary: Don’t wait for a loan rejection to look at your report. Checking it is like a “Health Check-up” for your money—do it regularly to stay fit!

Quick Checklist: What to Look for Today

-

Personal Info: Is your PAN and Phone Number correct?

-

Account Status: Are all your closed loans marked as “Closed” or “Settled”?

-

Enquiries: Do you recognize every bank that searched for your name?

Improve Your Score: The ‘Financial Dost’ Action Plan

Improving your credit score isn’t an overnight miracle, but in the era of weekly reporting, you can see progress much faster than before. Here are the four most effective ways to move that needle:

1. The ‘Golden Rule’: Pay on Time, Every Time

Your payment history is the biggest chunk of your score.

-

The Trick: Set up Auto-Pay for your EMIs and Credit Card bills. Even being late by 3 days can now be reported to the bureau within a week.

-

Pro-Tip: If you have an old “Settled” or “Written Off” account, try to pay the remaining balance and get a “No Dues Certificate” (NDC) to clear your name.

2. Control Your ‘Credit Hunger’

Every time you apply for a new credit card or loan, the bank does a “Hard Enquiry.” Too many of these make you look desperate for cash.

-

The Strategy: Space out your applications by at least 3 to 6 months. If you want to compare rates, use “Soft Check” tools (like the ones on our site) that don’t hurt your score.

3. The 30% Utilization Rule

Just because your credit card has a limit of ₹1 Lakh doesn’t mean you should spend it all.

-

The Goal: Try to keep your total credit card usage below 30% (e.g., spend only ₹30,000).

-

The 2026 Hack: Because of weekly reporting, if you have a big expense, pay it off before the bill is even generated. This keeps your reported utilization low and your score high.

4. Don’t Be Too Quick to Close Old Cards

The “Age of Credit” matters. That old credit card you’ve had since your first job? It’s helping your score by showing a long, stable history.

-

The Advice: Keep your oldest credit accounts active, even if you only use them for a small monthly subscription. It proves you’ve been “reliable” for years.

Ready to start? The best day to start improving your score was 6 months ago; the second best day is today. Check your report, fix the errors, and watch those numbers climb! If you want to increase your credit score quickly, read our complete guide on improving your credit score in India.

Financial Guides and Resources

On this website you will find helpful guides including:

• How to improve your credit score

• Best credit cards in India

• Personal loan eligibility tips

• Understanding EMI calculations

• Managing debt responsibly

Our goal is to provide reliable financial information that helps you build a stronger credit profile.

Disclaimer

The information provided on this website is for educational purposes only. We are not a financial institution or credit bureau. Users should verify information with official credit reporting agencies before making financial decisions.